Immigration Law

Not long ago, an investor came to me with what looked like a strong E-2 case. The business was viable. The investment amount was more than sufficient. The business plan was polished.

But there was one problem — he could not clearly document where the money came from.

That single issue nearly derailed the entire case.

Source-of-funds documentation is the most overlooked element of the E-2 visa process — and in my practice, it is also the most common reason otherwise strong cases run into serious trouble. Consular officers and USCIS adjudicators do not simply confirm that money exists in a bank account. They trace it backward, step by step, looking for gaps, inconsistencies, and red flags that most applicants never anticipate.

I have handled E-2 cases involving personal savings, property sales, family gifts, business distributions, and situations where the majority of the investment capital was borrowed. Each source carries its own documentation burden, its own pitfalls, and its own level of scrutiny. Knowing how adjudicators actually evaluate these packages — and where cases typically break down — is what separates approvals from 221(g) refusals that stall your plans indefinitely.

Most E-2 applicants spend the bulk of their preparation energy on the business plan. That makes sense on the surface — the business plan tells the story of what you intend to build. But in my practice, I focus heavily on the financial documentation side, because that is where most E-2 applications actually succeed or fail.

Consular officers reviewing source-of-funds evidence are not evaluating your entrepreneurial vision. They are conducting a financial audit.

The legal standard sounds simple. Under 8 CFR § 214.2(e)(12), investment capital must be placed at risk in a commercial sense, the investor must demonstrate possession and control of the funds, and the funds must not have been obtained through criminal activity. The Department of State's Foreign Affairs Manual expands on this significantly, requiring consular officers to examine the "original source of funds" and verify who has had possession and control throughout the chain.

What this means in practice: a bank statement showing $200,000 in your account tells the officer almost nothing. They want to know how that $200,000 got there, where it was before that, and whether every step in its journey can be verified with documentation.

If you are considering an E-2 investment and have not yet thought carefully about how you will document the origin of your capital, I strongly recommend making that the first conversation you have with an immigration attorney — before you sign a lease, purchase equipment, or transfer money internationally.

The statutory basis for the E-2 visa under INA § 101(a)(15)(E)(ii) requires the investor to develop and direct an enterprise in which they have invested, or are actively investing, a substantial amount of capital. While the statute does not use the phrase "lawful source," the requirement is built into how "capital" is defined and has been strictly enforced through decades of regulatory interpretation and case law.

Three principles drive every source-of-funds adjudication:

Lawful origin. The capital must come from a legitimate source. The landmark decision in Matter of Ho (1998) established that a bank letter or statement showing a deposit is not, by itself, sufficient. Officers expect corroborating documentation that explains how the funds were earned or acquired.

Traceability. The investor must show an unbroken chain from the original source to the U.S. business account. Matter of Izummi (1998) — originally an EB-5 case — is routinely applied in E-2 adjudications for the principle that the complete path of funds must be documented.

Possession and control. The investor must show they owned and controlled the funds throughout. This becomes particularly critical in cases involving gifts, business distributions, or funds routed through intermediaries.

These are not abstract legal principles. They translate directly into the documents a consular officer expects to see — and the questions they will ask when those documents are missing.

Every source of investment capital carries its own evidentiary burden. In my practice, four categories account for the vast majority of E-2 source-of-funds scenarios.

Personal Savings and Employment Income

This is the most straightforward source on paper, but it still requires a documented accumulation narrative. The officer needs to see that your savings grew over time in a way consistent with your reported income.

I caution clients against assuming that a healthy bank balance speaks for itself. A sudden, unexplained spike in your account — even if the money is legitimately yours — raises immediate questions. The foundation typically includes several years of tax returns, employment contracts, pay records, and bank statements showing deposits consistent with reported earnings.

Sale of Real Property

Property sales are common, but they introduce a layer of complexity many applicants overlook. Documenting the sale itself — the purchase and sale agreement, closing statement, title transfer, and capital gains filings — is only the beginning.

Officers may look back to the original purchase of the property. If you bought a home for $150,000 ten years ago and sold it for $400,000 today, the officer may ask how you funded the original purchase. I advise clients to be prepared to document not just the recent sale but the history behind the asset itself.

Gifts from Family

Gift-based funding is permissible, but it attracts heavy scrutiny — and this is the area where I see documentation go wrong more than almost any other.

A valid gift must be unconditional, with no expectation of repayment. The documentation requires a formal gift affidavit confirming the relationship and the absence of any repayment obligation. Critically, it also requires documentation of the donor's finances — their identification, tax returns, and bank statements showing they had the lawful means to make the gift.

Timing matters enormously. A large gift made shortly before filing is treated with deep suspicion as a potential "disguised loan." The closer the gift is to the application date, the more aggressively the officer will probe.

I cannot overstate how often I see gift letters that are vague, poorly drafted, or missing the donor's supporting financial documentation entirely. A one-paragraph letter saying "I gave my son $100,000 as a gift" does not meet the standard. I advise every client using gift funds to treat the gift documentation package with the same rigor as their own financial evidence — because that is exactly how the officer will evaluate it.

Business Profits

When capital comes from a business the investor owns, the officer needs to see that funds were lawfully distributed from the entity to the investor personally. Corporate earnings in a business account are not the same as funds in the investor's possession and control.

This requires articles of incorporation, financial statements, corporate tax filings, and records of the specific distribution — salary, dividends, or owner's draw — that moved the money from the business to the investor's personal account. The gap between "my company earned this money" and "I personally received and control this money" is exactly where officers focus their review.

One of the most common questions I get is whether borrowed money qualifies. The answer is yes — but the structure matters critically.

The principle from Matter of Walsh and Pollard (BIA 1988) establishes that investment funds do not need to be fully spent prior to filing if they are irrevocably committed. A loan qualifies as legitimate E-2 capital when the investor has personally guaranteed it or secured it with their own assets — for example, a mortgage on property the investor owns.

What does not qualify: a loan secured by the assets of the U.S. business itself. If the business you are investing in is the collateral, the capital is not considered "at risk" in the way the regulations require.

In a recent case I handled, the majority of the investment capital was borrowed. While I generally advise caution with this structure, careful documentation of the loan terms, the personal assets securing the debt, and the investor's ability to service the loan allowed the case to be approved. The difference was preparation — every element of the borrowing arrangement was documented and presented in a way that anticipated the officer's concerns before they became objections.

If you are considering a loan-based E-2 investment, I strongly recommend working with an attorney before committing to the financing structure. The line between qualifying and disqualifying loan arrangements is technical, and getting it wrong means a denial.

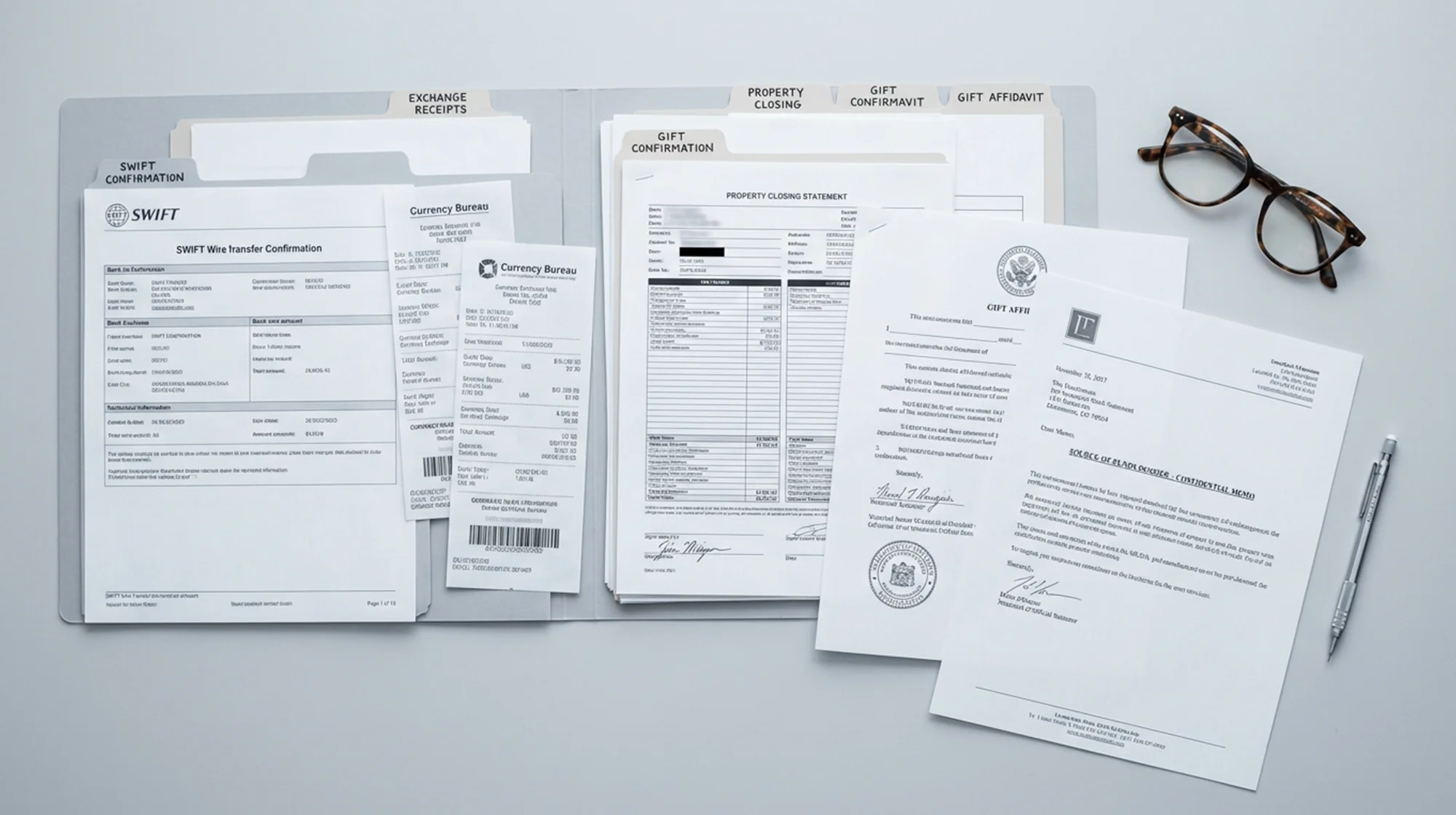

Beyond proving where your money originated, you must demonstrate how it traveled from that origin to your U.S. business account. This is the tracing requirement, and officers — particularly at USCIS — apply it with the rigor of a forensic audit.

A typical chain for foreign earnings might follow this sequence: payroll records confirm income, bank statements show consistent deposits, a withdrawal is documented, a currency conversion receipt shows the exchange, a SWIFT or MT103 wire transfer record confirms the international movement, and a U.S. bank statement shows the deposit into the business account. Every link must be documented.

In my experience, three scenarios break the chain most often:

Commingling. When investment funds are mixed with other undocumented money in a single account, it becomes impossible to demonstrate that the specific dollars reaching the U.S. business are the same dollars that were lawfully sourced.

Unexplained cash deposits. Large cash deposits without a clear accumulation trail trigger anti-money laundering concerns. Even if the cash is entirely legitimate, the absence of documentation creates a presumption problem that is extremely difficult to overcome after the fact.

Amount inconsistencies. When a wire transfer amount does not match the corresponding bank statement or business plan projections, officers notice. Even small discrepancies caused by fees or exchange rate fluctuations need to be explained and documented.

After handling numerous E-2 cases, I can say that most source-of-funds problems are not caused by the funds themselves. The most common breakdown I see is not illegal money — it is incomplete documentation of otherwise legitimate funds.

Insufficient effort. I often see investors — and, frankly, some attorneys — treat source of funds as an afterthought. They assemble a few bank statements, attach a brief letter, and assume it will be enough. That approach is one of the fastest ways to receive a 221(g) refusal.

Poorly drafted gift letters. This is one of the most consistent problems in my practice. The affidavit is vague or informal, the donor's financial documentation is missing, or the letter fails to explicitly state that no repayment is expected. A weak gift letter does not just fail to help — it actively raises suspicion.

Over-inclusion of irrelevant documents. More paper is not better. I caution against submitting hundreds of pages of loosely related financial records without a clear organizational narrative. A disorganized package signals that the applicant's legal team does not fully understand what the officer is looking for. Every document should have a purpose, and that purpose should be obvious.

Gaps in the timeline. If the narrative says funds came from a property sale in 2023 but bank statements skip from January to June of that year, the officer will notice.

These are the kinds of issues that a thorough pre-filing review catches and corrects. Left unaddressed, they result in a 221(g) refusal or outright denial — and at that point, recovery is significantly harder.

Understanding the officer's perspective changes how you approach preparation. In my practice, I build every source-of-funds package with one question in mind: can the officer follow the money from origin to investment without having to ask a single question?

When an officer has questions the documentation does not answer, the typical outcome is a 221(g) hold while additional evidence or administrative processing is completed. This is not a final denial, but it delays the case significantly and puts you in a reactive position.

Scrutiny levels vary by consular post — sometimes dramatically. In my experience working with investors applying through different posts, I have seen significantly stricter standards in certain jurisdictions, particularly where financial transparency norms differ from U.S. expectations. Applicants from countries with less standardized banking systems or where business records follow different accounting conventions often face additional documentation challenges that must be anticipated and addressed proactively in the initial filing.

The doctrine of consular nonreviewability means visa denials by consular officers are generally not subject to judicial review. The exceptions are extremely narrow. This underscores why getting the documentation right the first time matters so much — there is often no meaningful appeals process if the officer is not persuaded.

A properly prepared source-of-funds package is not a stack of financial documents. It is a structured legal argument, organized to guide the officer through your financial narrative step by step.

The foundation is a detailed cover letter or "Source of Funds Summary" that functions as a roadmap. I draft these to explain, in plain language, where the capital originated, how it was accumulated, and how it moved to the U.S. business account. Done well, it eliminates guesswork and preemptively addresses potential questions.

Visual aids — flow charts and timelines illustrating fund movements — are increasingly valuable, particularly in cases with multiple sources or multi-step international transfers. I use these to give the officer an immediate framework for evaluating the supporting documents.

In cases involving complex accumulation histories or foreign business distributions, expert letters from forensic accountants or CPAs can bridge gaps and authenticate records that may be unfamiliar to a U.S.-based officer.

Every foreign-language document must be accompanied by a certified translation. Every affidavit must be properly notarized. These are procedural basics, but failing to meet them creates unnecessary friction — and in adjudication, friction is never your friend.

This level of preparation is what separates applications that move smoothly toward approval from those that stall. It requires understanding what officers look for, how they evaluate evidence, and where cases typically break down — knowledge that comes from handling E-2 cases regularly.

Source-of-funds documentation is where E-2 cases are won or lost — often before the consular interview even begins. The legal standards are technical, the scrutiny is real, and the consequences of a weak package range from months of delay to outright denial with limited recourse.

Every investor's financial picture is different, and the documentation strategy for personal savings looks nothing like one involving a property sale, a family gift, or borrowed capital. Getting this right is not about assembling paperwork — it is about building a case that answers the officer's questions before they ask them.

If you need guidance for your E-2 visa case, contact me at SG Legal Group. My team and I will help you navigate the process with clarity and confidence. Consultations are available in English, Russian, or Romanian. Call 410-618-1288 or schedule a consultation to discuss your specific situation.

Disclaimer: The information provided in this article is for general informational purposes only and does not constitute legal advice. Immigration laws and policies are subject to change, and individual circumstances vary. For advice specific to your situation, please consult with a qualified immigration attorney.

Oleg Gherasimov, Esq.

Stay informed with our latest articles and resources.